For most Canadians, your home is your single largest asset. Tapping into this reservoir of accumulated wealth is a good solution for cash-strapped seniors facing increasingly high living expenses. Fortunately, homeowners who own their home outright or who have a low mortgage balance can access some of the value they’ve amassed in their home without having to sell their property. A reverse mortgage, the financial vehicle that makes this possible, is a good solution for many cash-strapped, older Canadians.

What Is A Reverse Mortgage?

Maybe you’ve been wondering “what is a reverse mortgage?” A reverse mortgage is a type of home equity loan available to Canadians age 55 and older who have built up equity in their homes. This financial vehicle allows such homeowners to access a portion of that home equity to use as they see fit, for paying off debt, medical expenses, day-to-day living expenses and even vacations or trips. The amount of money you qualify for depends on the value of your home, home type and location, your age (and that of your spouse). The maximum you can receive is 55 percent of the equity value.

Unlike other mortgages and loans you’re also not required to make interest payments or payments towards the principal. You just need to keep current on your property taxes, your home maintenance, and insurance. The loan becomes due when you no longer reside in the home, either after your death, when you move or when you sell the property. At your death, your heirs have the choice of either paying off the loan and keeping the house or using the sale of the property for payment of the loan.

You, as the homeowner, remain on title of the property. There’s no mandate to move out of your home at any time. You can stay as long as you stay current on your taxes, maintenance and insurance. That’s true whether you take out your reserve mortgage at age 55 or later.

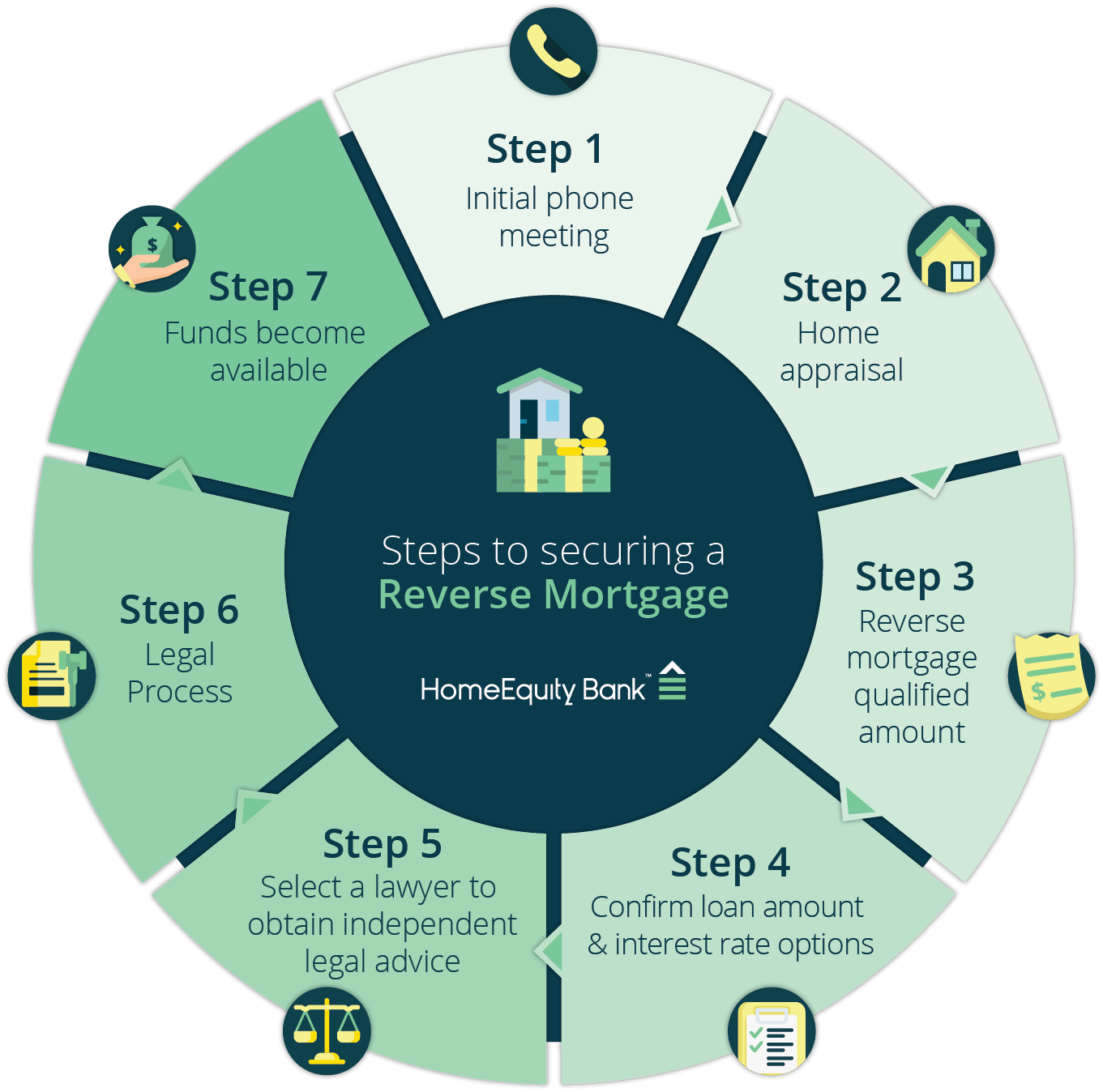

How To Get A Reverse Mortgage Loan

What is a reverse mortgage and how can you get one? In order to qualify for a reverse mortgage, you must meet a few criteria…

-

- You and your spouse must be at least 55 years of age.

- The property must be your primary residence.

- Your property must be of a certain type and in a location that HomeEquity Bank lends to.

CHIP Reserve Mortgage

So what exactly what is a reverse mortgage in Canada? Reverse mortgages in Canada are somewhat different from reverse mortgage products sold in the United States. All reserve mortgages in Canada are provided by HomeEquity Bank, the most popular of which is the CHIP Reverse Mortgage. This program has been helping older Canadian homeowners for more than 25 years. Homeowners can opt to get their money in a lump sum or as periodic advances.

How Is A Reserve Mortgage Better Than A Traditional Mortgage?

For older Canadians on a fixed income or with a limited amount of money coming in each month, a reverse mortgage can give you the funds you need to continue living comfortably without having to move or downsize. What’s more, you aren’t expected to make monthly mortgage payments to the bank.

A reverse mortgage is not the right choice for every Canadian homeowner age 55 or older looking for an extra source of monthly income. However, if you are a Canadian homeowner age 55 or over this financial product might be a good way for you to augment your monthly income.

So, if you’re wondering just what is a reverse mortgage and whether you meet the necessary requirements, perhaps it’s time to request a free guide.