The reverse mortgage has become an essential financial option for many Canadian retirees. Reverse mortgages are growing by over 28% annually and it’s easy to understand why. Retirees are increasingly house rich and cash poor. A combination of rising living costs, inadequate pension plans, increased health care expenses and longer life expectancy has led to many Canadian retirees struggling financially.

A reverse mortgage allows homeowners to cash in some of the equity in their home and use the money in any way they wish. It’s such a popular financial option because, unlike a regular mortgage, loan or line of credit, you don’t have to make regular payments on a reverse mortgage. This frees up much more of your retirement income.

Retirees use a reverse mortgage for a wide range of reasons, including paying off debt, financing health expenses, making accessibility renovations, helping out family members, or simply boosting their retirement income and their overall standard of living. You can find out more about how a reverse mortgage works.

While reverse mortgages in Canada have been available for over 30 years, there are still a lot of reverse mortgage myths and misconceptions. This article explores these myths and reveals the real truth about reverse mortgages.

Key differences between reverse mortgages in Canada versus the U.S.

Many of the reverse mortgage myths in Canada come from confusion with American products. These perceived reverse mortgage problems can sometimes persuade people not to take out a reverse mortgage in Canada. Here are some of the key differences between reverse mortgages in Canada versus the U.S.:

Maximum mortgage amount:

Canada: Up to 55% of the home’s value, thus helping to maintain equity in the home.

U.S.: A maximum of $625,500 and if the home’s value is under this limit, then the borrower is able to access a percentage.

Who is eligible?

Canada: Homeowners 55 years and older.

U.S.: Homeowners 62-65 years and older (depending on the company providing the reverse mortgage).

Approval Process for Reverse Mortgage

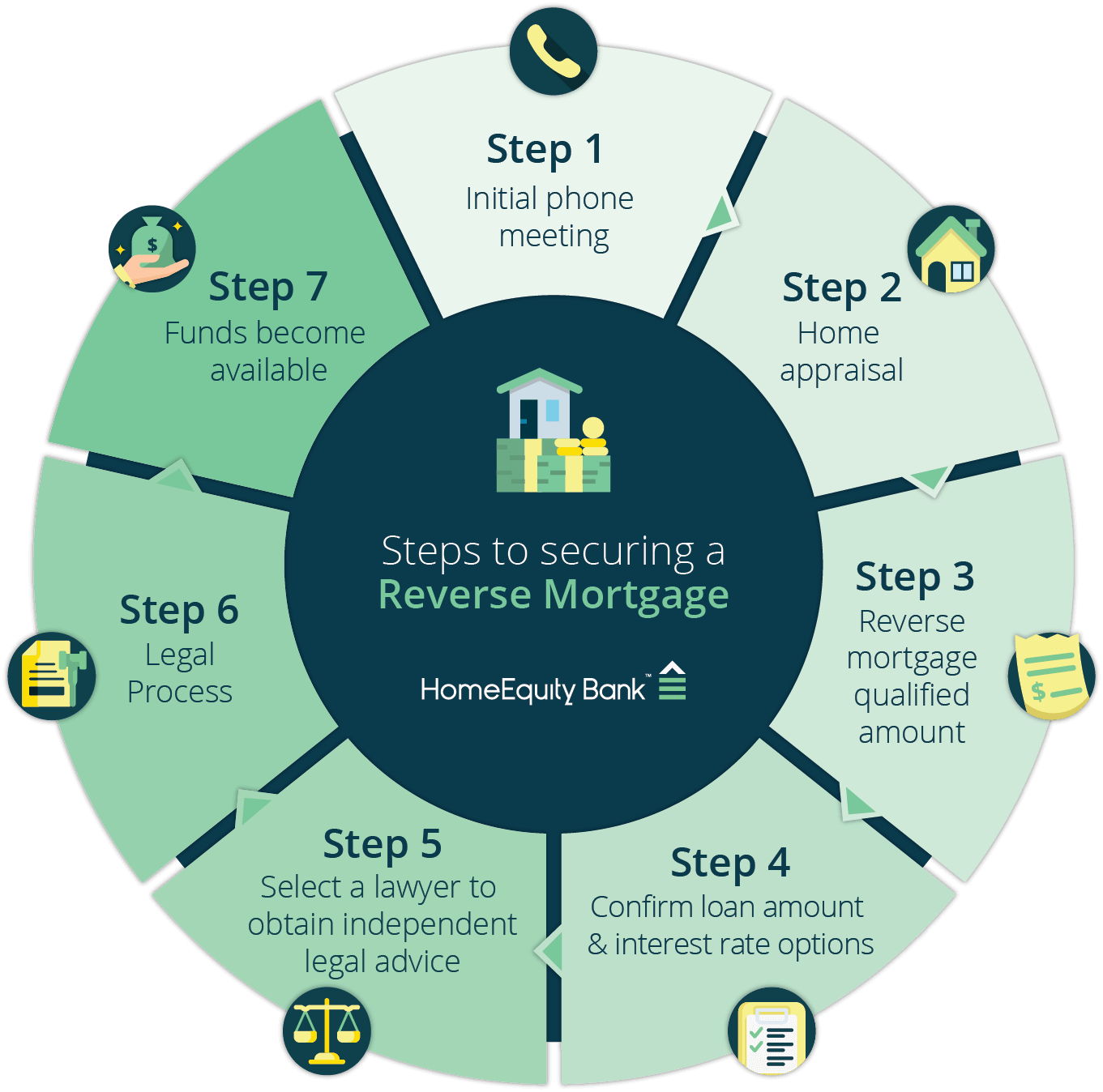

Canada: The borrower must seek independent legal advice before being approved for a reverse mortgage.

U.S.: In the U.S., the Consumer Financial Protection Bureau provides counselling to reverse mortgage applicants.

Costs Involved with Reverse Mortgage

Canada: You will have to pay fees for your independent legal advice, an appraisal fee and standard closing/admin costs. In most cases, these fees can be included in your mortgage loan. Typically, the only up-front cost is the appraisal fee.

U.S.: Mortgage insurance premiums, origination fees, third party charges, and servicing fees apply. The insurance premium in most cases is 0.5% of the loan amount but may vary with provider. While the origination fee is capped, it is calculated based on the value of the home.

- For example: for a $500,000 home, the origination fee would be $6,000, which is the maximum amount.

Tax implications

Canada: One of the common reverse mortgage myths is that you have to pay tax on the proceeds. This is not true in Canada: a reverse mortgage is tax-free cash and does not affect government benefits such as OAS or GIS.

U.S.: Advances are tax-free, but annuity (monthly) advances may be partially taxable.

Some of the common reverse mortgage myths and misconceptions

While reverse mortgages are highly regulated in Canada, this has not always been the case in other countries. This has led to the spread of myths regarding the CHIP Reverse Mortgage® problems that simply aren’t true. Below are details of the more common myths to give you a better idea of the real truth about reverse mortgages:

1. You no longer own your home

This is one of the most common reverse mortgage problems that simply isn’t true. You continue to own your home, hold title and have full control over it, just as you would with a regular mortgage. The bank cannot force you to sell and you can live there as long as you wish. Your only obligation is to keep your home well-maintained and pay your property taxes and insurance.

2. You end up owing more than your house is worth

This is also false. With the CHIP Reverse Mortgage from HomeEquity Bank, there is a guarantee1 that, as long as homeowners have met their obligations, they will never owe more than their home is worth. The truth about reverse mortgages is that over 99% of HomeEquity Bank’s customers have equity in their home when they come to sell it, and, on average, they have well over 50% of the value of their home left to enjoy after repaying the loan.

This is why there are rarely CHIP Reverse Mortgage problems for heirs; after the house is sold and the mortgage paid off, there is typically a large amount of money left over.

3. You can only apply if you’re 62 or over

While this is the case in some countries, in Canada, the CHIP Reverse Mortgage is available to Canadian homeowners age 55 and older. Of course, the older you are when you apply for the loan, the more money you are likely to qualify for.

4. You can be evicted from your home if you don’t make payments

This is one of the most common reverse mortgage myths and is absolutely false. You are not obliged to make any monthly payments at all, so you can’t miss any.

5. It’s very expensive to arrange a reverse mortgage

This is also incorrect. As with many conventional mortgages, you will need to pay for an appraisal of your property and independent legal advice. Other than that, the only up-front cost is a one-off closing and admin fee. Compared to alternatives, such as downsizing, a reverse mortgage is a much more affordable option.

6. Interest rates are really high compared to traditional mortgages

One truth about reverse mortgages is that, in general, the interest rates are often a little higher than a conventional mortgage, but not excessively so. Reverse mortgages are not conventional mortgages, so they have slightly higher rates because you don’t have to make monthly mortgage payments.

Many retired Canadians cannot afford monthly mortgage payments and many of them may not even qualify for a regular mortgage, based on income. Reverse mortgages require no regular mortgage payments and qualification is typically easier than with a conventional mortgage.

7. Your children will lose the family home

This is a perceived reverse mortgage problem for heirs that is not true. Your heirs have the opportunity to pay off your reverse mortgage after you pass away and keep the property. Plus, we guarantee1 that they will never owe more than the fair market value of the home.

8. You have to take out mortgage insurance

This is another reverse mortgage problem that is only true in other countries. When you take out a CHIP Reverse Mortgage, we don’t ask you to pay for mortgage insurance.

Some important facts about reverse mortgages

Now that we’ve debunked some of the common reverse mortgage myths, here are some facts that will help you to decide if this is the right financial solution for you:

1. You don’t have to make any regular mortgage payments

The key difference between a reverse mortgage and other mortgages and home equity loans is that you are not required to make any regular monthly mortgage payments with a reverse mortgage. This allows you to cash in a large part of your home’s equity without any negative impact on your retirement income.

2. What happens when you move, sell or pass away

The reverse mortgage is a portable loan; therefore, if you move, you can take it with you. However, if you decide you would then like to pay off your reverse mortgage or if you are moving into a home where you are not the principal owner, these are the next steps.

- If you decide to move from your principal residence, you will have 180 days to settle the loan with HomeEquity Bank. If you are moving to a nursing home or a care facility, you can get 50% off for the pre-payment amount (if applicable). If you decide to sell your home and end your reverse mortgage, just like with a traditional mortgage, you will be required to settle the loan by the closing date.

- If one of the homeowners passes away, the spouse or the other person on title can continue to live in the home without having to settle the loan. However, once both homeowners have passed away, the executor must provide HomeEquity Bank with a death certificate as soon as possible.

- One of the myths surrounding reverse mortgage problems for heirs is that they will be landed with a big bill when you die. This is simply not true. Once your home is sold, the loan is paid off with the proceeds and your heirs receive the remaining amount of equity. Your estate has 180 days after the notice of death to settle the loan.

3. What happens if you or your spouse were to pass away before the loan is paid

Another common reverse mortgage myth is that if one person dies, their spouse is forced to move out. This is not the case. The surviving spouse is under no obligation to move out or make any payments until they move or sell the home.

4. The fees that apply for a reverse mortgage

Similar to a traditional mortgage, there are some fees to arrange a reverse mortgage:

- An appraisal fee to determine your home’s value and therefore how much we will lend to you.

- Fee for independent legal advice – this is for the benefit and protection of you, the homeowner(s).

- An administration fee can be $1,795 – $1,995. This fee can be paid from proceeds of the reverse mortgage. With a traditional mortgage, there can be other fees similar to this, such as brokerage fees.

5. Reverse mortgage interest rates

Interest rates on reverse mortgages mirror the rates charged on other home equity loans. They are usually somewhat higher than the rates charged for a line of credit because you are not required to make monthly payments or repay the loan until you move or sell your home.

You can choose from a number of terms, such as three-year and five-year and can choose fixed or variable rates. You can see our reverse mortgage rates.

6. HomeEquity Bank customers recommend their CHIP Reverse Mortgage

According to a recent survey by HomeEquity Bank, 94% of their reverse mortgage customers would recommend this type of loan to others.

7. Reverse mortgages are a secure financial product

Reverse mortgages have been available in Canada for over 30 years. HomeEquity Bank, one of the only national providers of reverse mortgages in Canada, is a federally regulated, Schedule 1 Canadian bank and subject to strict financial rules.

DOWNLOAD OUR FREE RESOURCE

Check out the most important questions answered on Reverse Mortgage

Reverse mortgages: an ideal financial solution for many Canadians

As we’ve seen above, many of the perceived CHIP Reverse Mortgage problems are simply not true. However, one key truth about reverse mortgages is that they provide security for many Canadians during their retirement, as well as reduced financial stress and a better quality of life.

To find out how much you could qualify for, try our reverse mortgage calculator, or call us at 1-866-522-2447.

[1] The guarantee excludes administrative expenses and interest that has accumulated after the due date.